Emergency Funds for Freelancers and Gig Workers

Ever look at your bank balance and think, “If one more unexpected expense pops up, I’m in trouble”? Trust me, I get it. That uneasy feeling is especially common when you’re juggling part-time gigs or bringing in sporadic income. A freelancer emergency fund can be your ultimate safety net—helping you cover surprise bills, maintain peace of mind, and keep building the life you want without living in constant fear of the next dry spell. Let’s walk through how you can make it happen, step by step.

Understand The Freelancer Emergency Fund

Building an emergency fund as a freelancer is a whole different ballgame than it is for folks with stable nine-to-five jobs. You might not have a predictable paycheck, guaranteed benefits, or an employer-sponsored safety net. Instead, your livelihood depends on charging for completed projects, hustling for new clients, and sticking to a budget that can change every month.

Why Being Prepared Matters

Think of your freelancer emergency fund like a personal cushion that softens life’s financial blows. Without it, a single delayed payment or unexpected medical bill could trigger an avalanche of stress. But when you have that rainy-day stash, you can:

- Cover urgent repairs for your car or essential equipment

- Keep up with monthly bills when client payments arrive late

- Replace a broken laptop or piece of technology you rely on

- Tackle personal emergencies without sending your finances into chaos

It’s not about hoarding money out of fear—it’s about giving yourself room to breathe so you can focus on doing your best work.

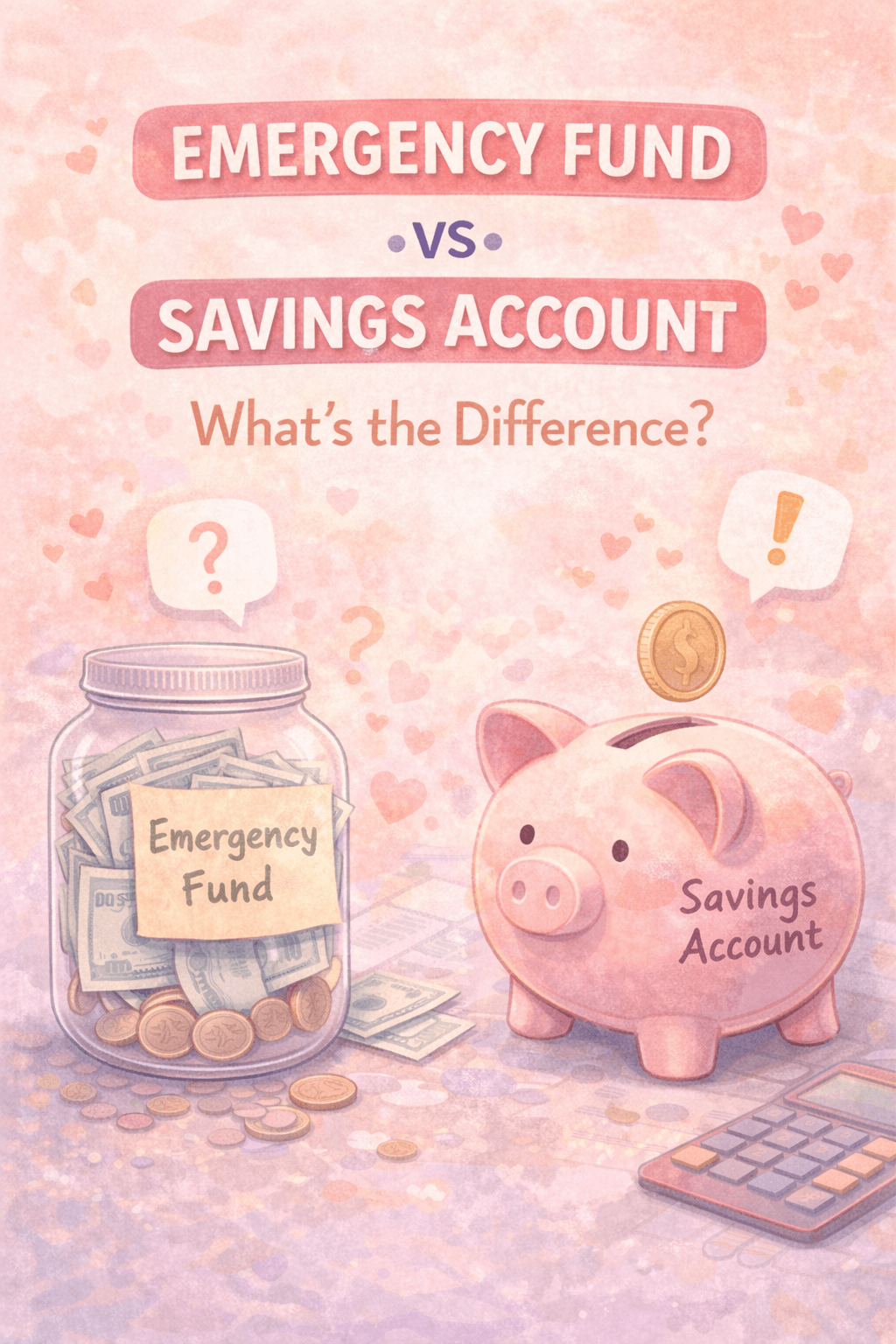

How This Fund Differs From Traditional Savings

An emergency fund is not your regular savings account. You’re not saving for a vacation, a new laptop, or even a dream house someday. This is money you tuck away for worst-case scenarios, so it needs to be accessible, ideally in a separate high-yield savings account. When you have a dedicated fund, you’re less likely to “borrow” from it for non-emergencies.

Also, consider any unique costs your freelance work might demand. Unlike typical employees who might have company-sponsored resources, you have to think about your own gear, health insurance premiums, and short-term cash flow gaps. In other words, this fund isn’t just personal—it also protects the very tools and resources you rely on to earn a living.

Figure Out Your Exact Needs

The first big question is: how much should you save? There’s no one-size-fits-all number here, because every freelancer’s life is different. You may have big monthly overheads if you lease a workspace, or maybe you’ve got relatively low living costs but a large family to support. Let’s piece it all together.

Estimating Your Monthly Costs

Start by listing all of your core expenses—rent, utilities, groceries, healthcare, phone bills, and any other recurring payments. Calculate an average of the last three to six months to get a decent sense of your usual baseline. Then, add in smaller items you might overlook:

- Subscriptions (software, streaming services, gym memberships)

- Transportation costs (fuel, public transit passes, occasional rideshares)

- Professional expenses (website hosting, online courses to upskill)

If your expenses vary, pick a realistic midpoint number, rounding slightly up to be safe. It’s better to budget for a bit more than you need than to come up short.

Factoring In Business Overheads

Freelancing sometimes blurs the line between personal and professional spending. If you’re running your own show, you might need to pay for special apps, social media scheduling tools, or hardware upgrades. Be honest with yourself about these essentials. If you skip them, your freelance gig might suffer, so they’re part of any effective freelancer’s emergency fund.

For example, let’s say you rely on a smartphone to coordinate gig work. If your phone suddenly dies, that’s an immediate emergency you need to address to keep your income flowing. So consider setting aside a bit extra for business emergencies, too.

Deciding On The Number Of Months

Most financial experts suggest saving three to six months’ worth of expenses. But for freelancers, it may be smarter to aim higher—closer to six to nine months if you can. A longer runway allows you to navigate lean times or periods when you’re searching for new clients.

Of course, hitting that target might feel intimidating, especially if you’re used to living paycheck to paycheck. If that’s the case, it might help to explore ways to build a paycheck to paycheck emergency fund and scale up from there. Whatever your approach, start with a bite-sized goal—like saving one month’s worth of expenses—and build as you go.

Build A Consistent Savings Habit

All right, so you’ve crunched the numbers and have a ballpark figure in mind. Next up is creating a habit of actually layering that money into your emergency fund. It’s one thing to promise you’ll save a chunk of each payment, but it’s another to follow through—especially when invoices can show up at random times.

Pay Yourself First

One tried-and-true strategy is to treat your emergency fund contribution like a non-negotiable bill. As soon as you get paid, you funnel a set percentage (for instance, 10% or 15%) into your savings, before you allocate anything else. This method helps you avoid the trap of “I’ll contribute whatever is left at the end of the month,” because, let’s be honest, there’s rarely anything left at the end of the month.

Try automating the process, too. Many online banks let you set up automatic transfers from checking to savings on specific dates or whenever a deposit hits. Removing the element of “should I or shouldn’t I?” simplifies everything.

Break It Down Into Micro-Goals

Saving a hefty sum can feel like climbing a mountain. Instead, chunk it into smaller milestones. For instance:

- Aim to save $1,000 first

- Then work toward saving one month of expenses

- Next, two months, and so on

Each time you reach one of these mini-goals, celebrate it—maybe with a small treat like a fancy latte or an hour of well-deserved downtime. These little rewards help anchor your motivation and remind you that slow, steady progress is worth patting yourself on the back for.

Be Realistic With Your Timeline

If you push yourself to put away too large a portion of your income, you risk falling behind on other obligations or dipping into credit card debt. That can undo all the progress you’re making. Strive for a healthy savings rate that won’t leave your basic needs in jeopardy. If you can comfortably save 10% of each payment, that’s fantastic. If it’s only 5%, that’s still better than 0%. Over time, you can adjust upward as you earn more.

Manage Irregular Income Streams

Freelance life can sometimes feel like feast or famine: one month you’re booked solid, the next you’re scrounging for work. That’s exactly why a freelancer’s emergency fund becomes your lifeline during those inevitable dips. But how do you manage your money when everything’s so unpredictable?

Project Future Earnings (As Best You Can)

Forecasting your earnings can be tricky, but it helps to maintain a simple spreadsheet where you list each confirmed project and its expected payment date. Update this chart often—whenever a new job comes in or a big invoice clears. Even though it’s not as firm as a salary, having a rough idea of your upcoming income can guide how much you can afford to push into savings that month.

If you notice you have a lighter workload coming up, you might decide to save more aggressively while you’re flush with cash. Or, conversely, know when to tighten your budget so you don’t have to dip into your savings unnecessarily.

Set Aside Funds For Taxes

Don’t let Uncle Sam catch you off-guard. Many freelancers forget that a chunk of their income needs to be earmarked for taxes, especially if you’re not having anything withheld by an employer. It’s wise to maintain a separate tax account so you’re not pulling from your emergency fund come tax season. After all, taxes aren’t an “unexpected” expense, they’re just a painful reality if you haven’t planned for them.

Create A Buffer For Slow Months

You know the slump can come without warning—sometimes the clients you rely on simply go quiet for a while. This is where your emergency fund rides to the rescue, letting you float through a slow spell without racking up credit card debt or missing essential bills. If you’re managing multiple streams of revenue from various gigs, you might also look into our tips on how to handle a multiple income emergency fund, especially if one income stream temporarily vanishes.

Whether you decide to reduce expenses during the lean times or pick up a side hustle for extra cash, having at least a few weeks of runway in your emergency fund keeps you from making panic decisions—like taking on less-than-ideal clients at rock-bottom rates just to stay afloat.

Plan For Unique Challenges

Freelancers aren’t a one-size-fits-all group. Some of you might share bills with a partner, while others might be single and supporting kids on your own. Maybe you’ve got big family medical costs, or you’re transitioning from a stable job to full-time freelancing. Whatever your situation, adapt your plan so your fund truly suits your lifestyle.

Freelancing As A Parent

If you’ve got kids counting on you, budgeting gets a little more complicated. You need to consider childcare costs, potential medical bills, or even unexpected school fees. By factoring in some extra padding for child-related emergencies, you can avoid the heart-stopping scramble when a field trip expense, a sudden ER visit, or a new set of clothes arrives out of the blue.

Your emergency fund also helps you say “yes” to important family opportunities without worrying if it’ll break the bank. If you’re looking for more ways to plan ahead for children’s future money needs, check out our guide to kids emergency fund education.

Partnering With A Spouse

Sharing finances with a partner or spouse can both simplify and complicate emergency fund planning. On one hand, you have two incomes and potentially a broader safety net. On the other hand, you might have conflicting savings habits or different ideas about what “emergency” truly means.

Talk openly about your goals—do you want a single emergency fund for both of you, or separate savings for personal needs? Having a plan ensures you’re on the same page if financial surprises arise. For an in-depth look at tackling expenses together, consider exploring the ins and outs of a couple emergency fund.

Single Parent Or Sole Provider

Let’s say it’s just you, holding down the fort entirely on your own. You might need a higher fund target to feel fully secure, because there’s no spouse’s paycheck to lean on. And if you’re a single mom or dad, your finances might be especially tight when gigs slow down.

This is one of those times to think big with your fund—maybe aiming for closer to nine months of expenses instead of three or six. That might sound huge, but every contribution builds on the last. You can also check out ideas in our resource on a single mom emergency fund to see how other single parents make it work.

Keep Growing Your Cushion

Having that initial wave of relief once you hit your savings target is fantastic. But an emergency fund is never really “done.” Your life circumstances, income, and expenses will evolve, and you might find new ways to keep growing your cushion, fine-tune it, or protect it from being depleted prematurely.

Revisit Your Goals Regularly

Maybe at first you aimed for three months of living expenses because that felt ambitious enough. Now, imagine you’ve gotten a raise or picked up a steady new client. That’s your chance to push the bar a bit higher—maybe move up to four or five months of expenses. Revisiting your fund target at least once or twice a year prevents your safety net from lagging behind your changing lifestyle.

Consider Additional Financial Tools

As your earnings grow, you might look into other layers of financial security—like business insurance for freelance work, or a separate health savings account if you have a high-deductible health plan. These aren’t strictly “emergency funds,” but they can help cushion specific types of crises so you don’t drain your main stash for every unexpected cost.

Pro tip: If you’re dabbling in investments, just remember that money locked in stocks or retirement accounts isn’t as easy to tap for a sudden emergency. It’s wise to keep your emergency money liquid and stable, even if the returns aren’t as high as more aggressive investments.

Avoid Raiding Your Fund

Tempting as it can be to borrow from your emergency fund for that incredible Black Friday deal or a dreamy vacation, resist if it’s truly a non-emergency situation. The moment you blur that line, you’ll find more and more reasons to dip into those savings. Keep your fund labeled in your mind—and in your banking apps—as “For Emergencies Only,” so you don’t accidentally sabotage all your hard work.

Move Forward With Confidence

Remember, the key here is progress over perfection. As a freelancer, you’re already juggling the unpredictability of gig work, the demands of life, and the occasional nagging worry about finances. But with a solid emergency fund, you’ll be able to weather the storms with a little less panic and a lot more confidence. Sure, it takes time to build up that safety net, but every single dollar you set aside is a step toward financial stability.

You don’t have to do this alone, either. Look to friends, online communities, or mentors for encouragement. We’re all in the same boat in some way—learning how to manage money, keep our dreams afloat, and maintain our sanity in the process. Check in with yourself periodically: Are you still on track? Have your circumstances changed? What’s your next savings goal?

Above all, give yourself credit for caring enough about your future to take these steps. A freelancer’s emergency fund is more than a pile of cash—it’s your strong foundation in a world of shifting gigs and paychecks. It’s a quiet assurance that, no matter what comes your way, you’ll have your own back. And that, my friend, is worth every penny.

So let’s keep going, one deposit at a time. You totally deserve it. You’ve got this, and I’m right here rooting for you all the way.