How to Access Your Emergency Fund During a Real Crisis

If you’re ever in the position of accessing your emergency fund, chances are life just threw a pretty heavy curveball your way. It might be anything from sudden medical expenses to a job loss, and it can feel overwhelming—like you’re not quite sure which way is up. Take a deep breath. You have this resource for a reason, and we’re all in this together. Let’s explore a supportive, step-by-step way to handle those truly tough situations so you can secure the funds you need without creating even bigger worries down the road.

Acknowledge the Reality of Crisis

We’ll start by calling it what it is. A genuine crisis is not your everyday annoyance, like a flat tire that costs a little extra. It’s the kind of emergency that risks your family’s well-being if you don’t take action soon. Sometimes, we’re tempted to downplay the severity of our situation—telling ourselves we’ll make do or wait until things blow over. But the first step is to face the facts with compassion.

Recognize a True Emergency

- Sudden unemployment that halts your income

- Significant health complications (yours or a loved one’s)

- Urgent home repairs that threaten your safety

- A family crisis requiring immediate travel or support

If any of those ring a bell, it’s time to act. By acknowledging that you’re in a serious bind, you lay the groundwork for making thoughtful choices about your finances. The beauty of having an emergency fund is knowing you’ve given yourself an umbrella for a rainy day—and it’s raining right now.

Give Yourself Emotional Space

In moments of heightened stress, it’s easy to feel isolated. Trust me, you’re not alone here. We’ve all had those nights where we stare at the ceiling wondering how we’ll handle the bills, the kids’ needs, and maybe even the unexpected hospital visit. Before you proceed, take a moment to let yourself feel what you need to feel. Fear is natural, but it doesn’t have to stop you from taking control. Give yourself permission to admit, “Yes, this is scary,” and then choose to move forward step by step.

Understand the Purpose of an Emergency Fund

Your emergency fund is designed to be a safety net—the financial cushion that keeps you afloat when life’s storms roll in unannounced. Creating this buffer is often the first step many families take toward better preparedness. If you’re still in the process of building up your resources, check out our start emergency fund guide for tips on how to begin.

More Than Just Extra Cash

An emergency fund isn’t spare change. It’s money you intentionally set aside for real crises, helping you avoid high-interest debt or major financial setbacks. Whether you learn about it through a year-long challenge or simply stash away modest amounts each month, it’s one of the sturdiest financial pillars you can build for yourself and your loved ones.

Objective vs. Emotional Value

On the surface, your fund’s objective value is the balance in your account. But emotionally, it represents security, peace of mind, and the knowledge that you’re caring for your family’s future. In the darkest moments, that sense of security is a tremendous relief. By keeping perspective on both the numbers and the comfort it brings, you’ll appreciate why these funds matter so much.

Assess Immediate Needs vs. Long-Term Effects

When a crisis hits, there’s an intense urge to solve everything immediately. You might find yourself eyeing the full balance of your fund, itching to pull it all out just to make sure every base is covered. But hold on. Drawing more than necessary can set you back later, especially if your crisis continues or another one emerges before you’ve replenished. Let’s figure out a balanced approach.

Prioritize the Essentials

Start by listing out the immediate, non-negotiable needs:

- Housing (rent or mortgage)

- Groceries and necessary household supplies

- Utilities (electricity, water, internet if it’s critical for work)

- Medical costs

- Transportation expenses if necessary for income or health

These are items that directly impact your family’s safety and basic living standards. Once you know these must-haves, it’s easier to estimate how much money you truly need right now. Think of it as focusing on the essentials before touching anything else.

Weigh the Future Financial Impact

Let’s say you have a major medical bill looming. Of course you need to cover it, but is there a payment plan option that lets you spread out the cost instead of draining your entire fund at once? This might help you maintain at least some safety net remaining. At the same time, keep in mind potential interest charges or fees. Balance immediate relief (paying crucial bills) with protecting yourself from additional instability.

It’s a tricky dance, but the goal is preserving as much of your emergency buffer as you can. Think of your fund as a set of stepping stones across a stream. You want to make each step carefully so you don’t run out of stones halfway across.

Set Clear Guidelines for Access

One of the biggest stumbling blocks during a crisis is that bi g question: “When do I actually use these funds?” If emotions are running high, it’s easy to justify just about any expense as an “emergency.” Setting guidelines ahead of time can prevent that slippery slope. But if you’re already in a crisis, clarifying those rules now can still help you make level-headed choices.

Define Your Threshold

Some people consider any unexpected bill over $500 a crisis, while others might wait until a family member’s job is lost. Reflect on the scale of your emergency and the impact it has on your day-to-day life. If skipping payment endangers your home, your health, or your livelihood, that strongly indicates a “this is what the fund is for” scenario.

Those guidelines also serve as a reminder of what not to touch the money for: impulsive buying, discretionary spending, or everyday inconveniences. If you’re just short on rent once, is that your emergency fund’s job, or do you need to restructure your monthly budget or find a side income boost?

Protect Your Mindset

Letting yourself dip into your emergency fund too easily can form a habit. Before you know it, you’re treating the fund like a normal checking account. Being clear about your rules—ideally in a written format you can reference—keeps you accountable. You can even jot down these guidelines in a trusted financial emergency binder, which you maintain for moments exactly like this. That way, the next time you’re tempted to call something an emergency, you can hold it up to the benchmark you already set.

Find the Right Withdrawal Strategy

Now we get into the nitty-gritty: how do you actually pull out the money? The approach hinges on the type of account or accounts you use. You might have a dedicated high-yield savings account or even a safer stash at home.

Choosing the Right Account

We all have different ways of storing crisis funds. It might be:

- A high-yield online savings account

- A money market account

- Certificates of deposit (CDs) with penalty-free features

- Cash on hand in a secure place

Each choice carries pros and cons for how fast you can retrieve your money. For instance, an online savings account typically allows quick electronic transfers, but it might take a day or two to land in your checking account. Meanwhile, emergency cash at home is immediate, but you risk theft or natural disasters if it’s not well protected.

Partial vs. Full Withdrawals

Consider taking only what you need rather than cashing out the entire fund. This keeps some padding in reserve if your crisis drags on or if you face multiple emergencies back-to-back. Large lump-sum withdrawals can be tempting—who wants to keep going back to the well during a stressful period? But pacing yourself can ultimately save you from complete depletion.

Also, look into any emergency fund withdrawal rules specific to your financial institution. Some banks limit transfers or apply fees if you exceed certain monthly transaction counts. Knowing these rules beforehand can keep last-minute frustrations at bay.

Table of Common Withdrawal Methods

| Method | Speed | Potential Drawbacks | Best Use Case |

|---|---|---|---|

| Online Bank Transfer | 1-3 days | Transfer limits, possible fees | Most straightforward, widely available |

| ATM Withdrawal | Immediate | Daily withdrawal limits, bank fees | Quick cash for small-but-urgent bills |

| Bank Teller Visit | Same day | Branch hours, ID required, possible wait | Larger sums that need a bit more handling |

| Cash at Home | Instant | Risk of theft or damage to stash | Very immediate, covers quick essential costs |

Consider which method aligns with your current crisis. If time is on your side for a few days, maybe an online transfer is perfectly fine. If an urgent medical copay demands immediate cash, you might opt for an ATM withdrawal or your home stash.

Consider Safe Storage Options

It’s easy to assume all your emergency funds should live in a single savings account. But there can be strategic benefits to dividing your resources. For example, having part of your fund in a locked home safe (for small immediate needs) and the rest in a bank account can offer a blend of speed and security.

Diversification for Security

Think of it like not putting all your eggs in one basket. A single account might be compromised in a cyberattack or if the bank’s systems are down right when you need the funds. Having a portion accessible elsewhere means you’re less reliant on one source. However, we don’t want to go overboard and spread our funds so thin that we struggle to manage them. Two or three well-chosen locations is often enough.

Some folks also keep a small portion in digital payment apps in case they need to pay a bill online immediately or send money to a caretaker. Just remember that convenience can come at the cost of impulse spending if you’re not vigilant.

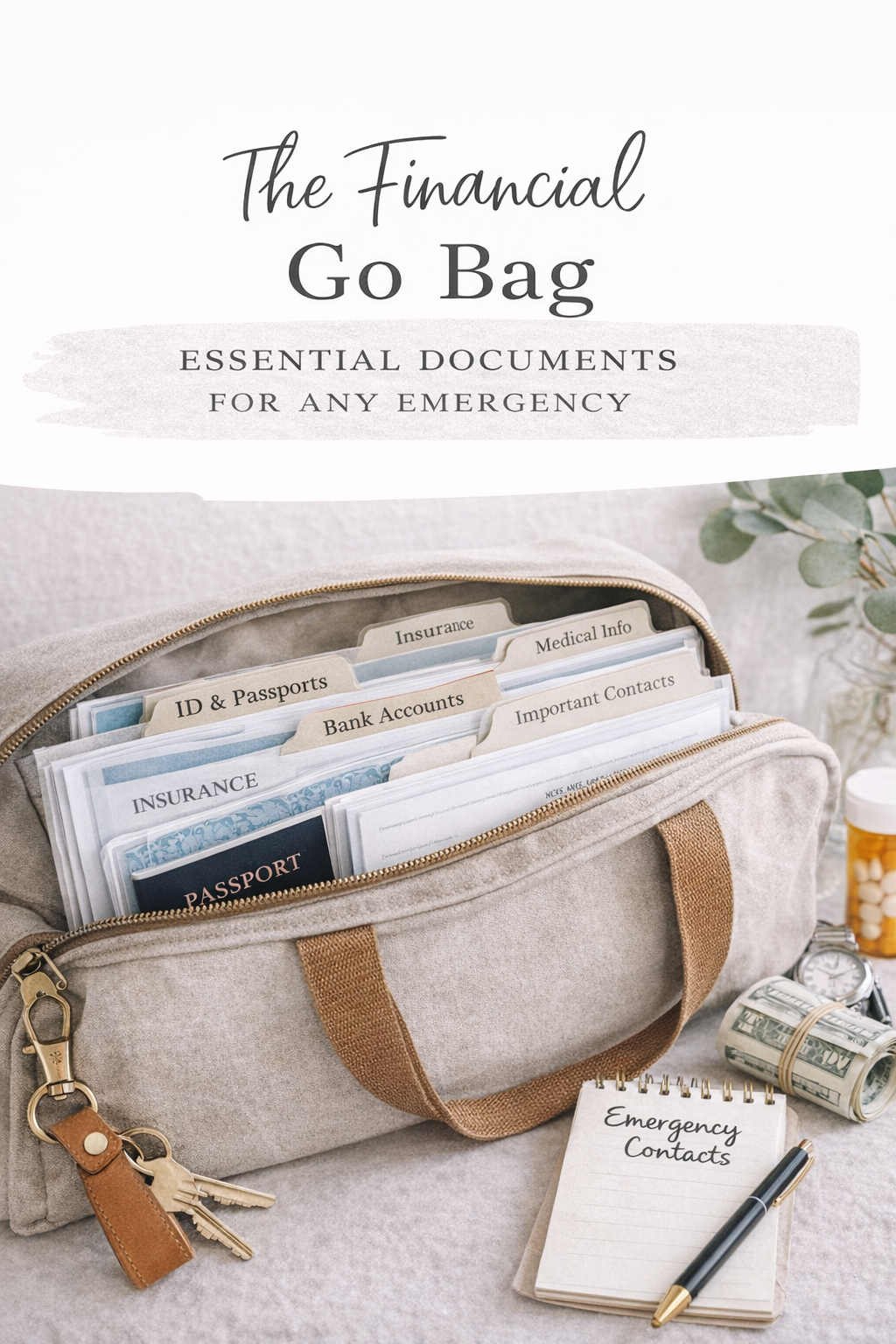

Using a “Financial Go Bag”

You might have a physical “go bag” with essential documents, cash, and a couple of emergency supplies. If you’d like to set one up, we’ve got tips in our financial go bag resource. The idea is to keep everything you’d need if you had to leave your home quickly. This stash could include copies of critical documents, your account information, extra keys, and a small sum of money. It’s just another layer of readiness and often pairs perfectly with your broader emergency plan.

Coordinate With Loved Ones

You’re not walking this path alone. If you have a partner, parents, siblings, or close friends who might be impacted by this crisis, it pays to communicate early. Let them know what’s happening and how you plan to navigate it. There’s no shame in admitting you’re under financial pressure. In fact, being open can relieve some of the emotional burden of a crisis.

Support and Accountability

Sometimes, a supportive conversation does wonders for your stress levels. Family or friends might pitch in with ideas, resources, or even just a listening ear. If you’re married or share finances with someone else, talk openly about how you’ll access the fund, what you’ll do if it depletes, and when you’ll decide to pause spending. Having this discussion in advance (or right now, if needed) helps avoid panic-driven transactions.

Delegating Tasks

If you’re too overwhelmed to handle all the calls, paperwork, or budgeting alone, assign some tasks to trusted individuals. Maybe your spouse can research ways to reduce certain bills while you tackle insurance claims. Or your sibling can help gather important paperwork for a financial preparedness checklist. This sense of collaboration can ease the weight on your shoulders.

Reflect and Rebuild

Once you’ve pulled through the crisis—or even while you’re still in it—it’s worth thinking about how to get back on your feet financially. Remember, the goal is not just to use the emergency fund but to ensure you can rebound from this episode stronger and more prepared.

Avoid Common Mistakes

When tension is high, it’s easy to make snap decisions. For instance, draining your entire fund when you could have spread out payments is a classic misstep. Another is forgetting to set money aside for the next emergency because you’re feeling relief after getting past the current one. Understanding potential pitfalls like these can help you avoid them. We have a resource on emergency fund mistakes if you want a deeper dive.

Start Rebuilding as Soon as Possible

If your fund is partly or fully drained, begin replenishing the balance immediately. Even if it’s a modest sum, it fosters the habit of saving again instead of letting your account remain at zero. You could try a 5 savings challenge or a year-long emergency fund challenge to gradually add funds without feeling stretched too thin. Every small deposit is a step closer to stabilizing your future. And yes, it might be a slow climb, but slow progress beats no progress.

Sustain Emotional Well-Being

There’s no denying that a financial crisis rattles you emotionally. It’s a cocktail of fear, guilt, frustration, and uncertainty. Even after you’ve taken steps to address the problem, you might still wrestle with lingering stress: “What if this happens again?” “Will I ever fully recover?” Those questions are normal, but they don’t have to own you.

Check-In With Yourself

We’re often so focused on finances that we forget our emotional self-care. It might help to talk with a counselor, especially if the financial strain is tied to other stressors like health issues or a rocky job market. Journaling can also be a gentle way to process what you’re feeling. Write down the day’s worries, future hopes, and one or two coping steps you tried. By putting your thoughts on paper, you’re giving them space to breathe instead of swirling endlessly in your head.

Celebrate Small Victories

Found a temporary side gig to bring in extra cash? Freed up $50 by swapping grocery brands? High five yourself—those are the small victories worth cheering. The key is to reinforce positive steps. You’re making changes and showing adaptability. Yes, the crisis is tough, but it’s not unbeatable.

Keep the Momentum Going

Staying prepared is an ongoing journey, not a one-time fix. Once you’ve navigated an emergency successfully (or even just survived it), you’re in a unique position to refine your approach. Consider it a lesson learned—one that might help you sail through the next storm more smoothly.

Review Your Crisis Response

Ask yourself how well your plan worked. Did you have enough in your fund to cover immediate needs? Were there any administrative headaches that slowed you down, like outdated contact information or forgotten passwords? If you uncovered hiccups, make the fixes right away. Update your emergency financial information storage so you’re not scrambling next time.

Adjust Your Fund Goals

Maybe you realized that your original emergency fund amount wasn’t quite enough for the type of crisis you faced. If so, reconfigure your savings to aim for an even more robust buffer, whether that’s a 3-month emergency fund or a larger target. Look at your budget and see if there’s room for incremental increases. Each time you bump up your savings, you’re making tomorrow a bit safer.

Revisit Long-Term Plans

Emergency funds are part of a bigger financial picture, which can include debt payoff, long-term investing, or family support. If you’re juggling debt, for instance, you might wonder where to direct your extra cash: emergency fund vs debt. You could prioritize high-interest debt while setting aside a smaller chunk into your fund, or focus on topping off your emergency stash first, depending on your comfort level. It’s all about balancing short-term stability with long-term growth.

Find Your Ideal Placement

Is your current bank still the best option? Or does switching to a different institution offer a better interest rate or quicker access? If you’re not certain where your emergency reserve should live, we have insights on where to keep emergency fund. The location should give you reliable, prompt access without tempting you to spend the money on non-emergencies. It’s a fine line, but finding the right account is definitely worth it.

Seek Progress Checkpoints

Your financial life will evolve, and emergencies will come in different shapes. Maybe you’re expanding your family, switching careers, or relocating. By checking in on your emergency fund every few months—especially after big life changes—you’ll keep it relevant to your current needs. This helps you catch potential issues before they balloon into another crisis.

Embrace Your Resilience

Even the most meticulously planned budget can’t shield you from every storm life brings. But having a clear plan to access and use your emergency fund makes the difference between a situation that derails your finances entirely and one you can recover from. Remember, crises are temporary, and you have the tools to move through them.

You’re human. You’ll make decisions that sometimes feel risky or uncertain. The beauty of having an emergency fund is that you’ve already given yourself a head start. By following these steps—identifying the crisis, setting guidelines, choosing the right withdrawal strategy, and aiming to rebuild—you can navigate the toughest moments with more confidence and peace of mind.

The fact that you’re here, reading this, shows you’re invested in your own financial stewardship. That’s an incredible leap forward. So when the tension rises and you feel that pit in your stomach, take heart. You’re not alone, and you have a solid plan to guide you. With each moment of action, you’re creating a more stable foundation for yourself and the people you care about. Lean into that knowledge, and keep trusting your abilities. You’ve got this.