Building Your Complete Financial Security Toolkit

Ever found yourself wondering what you’d do if a sudden medical bill popped up or your car decided to break down at the worst possible time? Trust me, you’re not the only one. Building a financial emergency preparedness kit might sound like a mouthful, but think of it as your safety net before life’s curveballs come speeding your way. When money worries strike, they can zap your energy and peace of mind faster than you can say “budget.” The good news? Putting together a toolkit for those just-in-case moments can help you stay calm and feel more in control. We’re going to walk through this process step by step, like two friends figuring out a plan together, so you’ll have everything you need to navigate unexpected financial hurdles.

It’s okay if you’ve felt intimidated by phrases like “emergency fund” or “financial plan.” After all, getting your finances in order can sound like you’re signing up for some complicated, day-long seminar. But breathe easy. You don’t need an MBA or a stack of spreadsheets taller than your fridge. You just need a clear process and a little support along the way. Let’s dig into what your complete financial security toolkit might look like, focusing on a core set of essentials that speak directly to your needs as a woman, a parent, or anyone eager to keep life’s nasty financial surprises at bay.

Below, we’ll explore each piece of the puzzle, one comfortable step at a time. By the end, you’ll have a roadmap to position yourself—and your family—for greater peace of mind. Ready? Let’s do this together.

1) Identify The Why

Sometimes our hesitation to prepare for emergencies isn’t about money at all—it’s about the emotional baggage we carry around it. Maybe you grew up in a household where financial stress led to arguments, or perhaps money conversations always felt taboo. When you’re on the fence about any big decision—especially one that involves setting aside cash each month—it helps to reconnect with why you’re doing it in the first place.

Reflect On Your Family’s Needs

Think about what truly matters most. Is it keeping a roof over your head during tough times? Ensuring your kids’ routines aren’t disrupted by looming bills? Or maybe it’s having the freedom to focus on healing if a medical crisis strikes, instead of being consumed by costs.Acknowledge Emotional Roadblocks

Fear and doubt can sneak up when you least expect it. You might worry you’re not earning enough to save, or you feel guilty prioritizing emergency prep over “fun” spending. Recognizing these emotions is the first step toward moving past them. We’ve all been there, questioning whether we’ll ever have enough. Believe me, you’re not alone.Shift Your Mindset To Empowerment

Instead of thinking, “This is too complicated, I’ll deal with it later,” try telling yourself, “I deserve a cushion that protects me and my family.” That mental reset helps you see preparation as a form of self-care—a forward-looking gift you’re giving to your future self.

Identifying your personal motivation is like laying the foundation for a house. Everything else in your financial emergency preparedness kit rests on having clarity and purpose. When you know the “why,” the “how” becomes a lot easier.

2) Establish An Emergency Fund

If there’s one piece of your financial toolkit that can lighten your load during a crisis, it’s your emergency fund. By emergency fund, we’re talking about a dedicated stash of money earmarked solely for those unexpected hits—like sudden income loss or a major car repair. Think of it as your financial airbag. You might never want to use it, but you’ll be forever thankful it’s there if you crash into an unforeseen expense.

Why Your Emergency Fund Matters

- Immediate Financial Cushion

This fund prevents you from sliding deeper into debt or hitting pause on important bills when an emergency happens. Whether it’s a burst pipe or a family member who needs help fast, having a buffer in place keeps stress more manageable. - Psychological Relief

There’s a mental freedom that comes with knowing you have resources on hand. It helps you sleep better and approach life’s uncertainties with greater confidence. - Sense of Control

For many women and families, financial security is about more than just balancing the checkbook; it’s about ownership over your choices. Having an emergency fund reflects that ownership.

Setting Realistic Targets

Experts often suggest aiming for three to six months’ worth of living expenses, but don’t let that standard intimidate you. If that figure feels out of reach right now, it’s okay to start smaller. Even a starter emergency fund of $1,000 is big progress if you’re new to saving. You can expand that fund over time—step by step. You might also explore a 5 savings challenge to consistently build momentum.

Getting Into The Habit

- Automate Your Savings

Set up a monthly or biweekly transfer from your checking to a separate savings account—perhaps the day after you get paid. That ensures you’re prioritizing your fund before you have time to talk yourself out of it. - Use A Specific Account

Keep emergency funds in an account that’s not overly accessible, so you’re not dipping into it for non-emergencies. Explore where to keep emergency fund options that align with your needs, whether it’s a high-yield savings account or a money market fund. - Celebrate Small Wins

Each deposit, no matter how large or small, is a step toward peace of mind. Acknowledge those mini-milestones to reinforce consistent saving.

Building your emergency fund isn’t about punishing yourself with a restrictive budget. It’s an investment in your stability and a key pillar for your entire financial emergency preparedness kit.

3) Gather Vital Financial Documents

Ever had to scramble for your car insurance details after a fender-bender? Or hunt down your health insurance info when you need urgent medical treatment? In an emergency scenario, the last thing you need is a frantic paper chase. That’s why storing essential documents in one safe, organized place can be a lifesaver.

Which Documents Are Essential?

- Insurance Policies

Keep copies of your health, homeowner’s, and auto insurance policies. Make sure you know exactly what these policies cover, so you’re not caught off guard by denied claims. - Bank and Investment Records

Store account numbers, contact information for your financial institutions, and any relevant statements or login instructions, especially if multiple people in your household might need access. - Loan or Mortgage Agreements

If you or your partner become sick or lose a job, you don’t want to be scrambling to figure out payment terms. Having these agreements on file can help you negotiate or adjust payments promptly. - Identification

Include photocopies of IDs, passports, birth certificates, and Social Security cards. In the midst of a crisis, every minute counts, and you don’t want to waste any rummaging for official documents.

Creating A Grab-and-Go System

You might store these documents digitally and in physical form. Going fully digital is convenient, but make sure you have secure backups, plus a system for easy retrieval if your device fails. As an extra layer of readiness, consider a portable financial go bag that holds physical copies, or a password-protected cloud folder you can access from anywhere.

Labeling and Checking

- Stay Organized

Label folders clearly: “Insurance,” “Bank Details,” “Loan Documents,” and so on. An emergency is no time to guess what’s inside each envelope. - Review Annually

Life changes happen (a new job, marriage, etc.), so schedule a yearly check. Updating these records ensures everything remains useful if you need them in a pinch.

Corral your paperwork into a single, secure spot. That alone can save hours of stress and confusion, making it an indispensable part of your financial emergency preparedness kit.

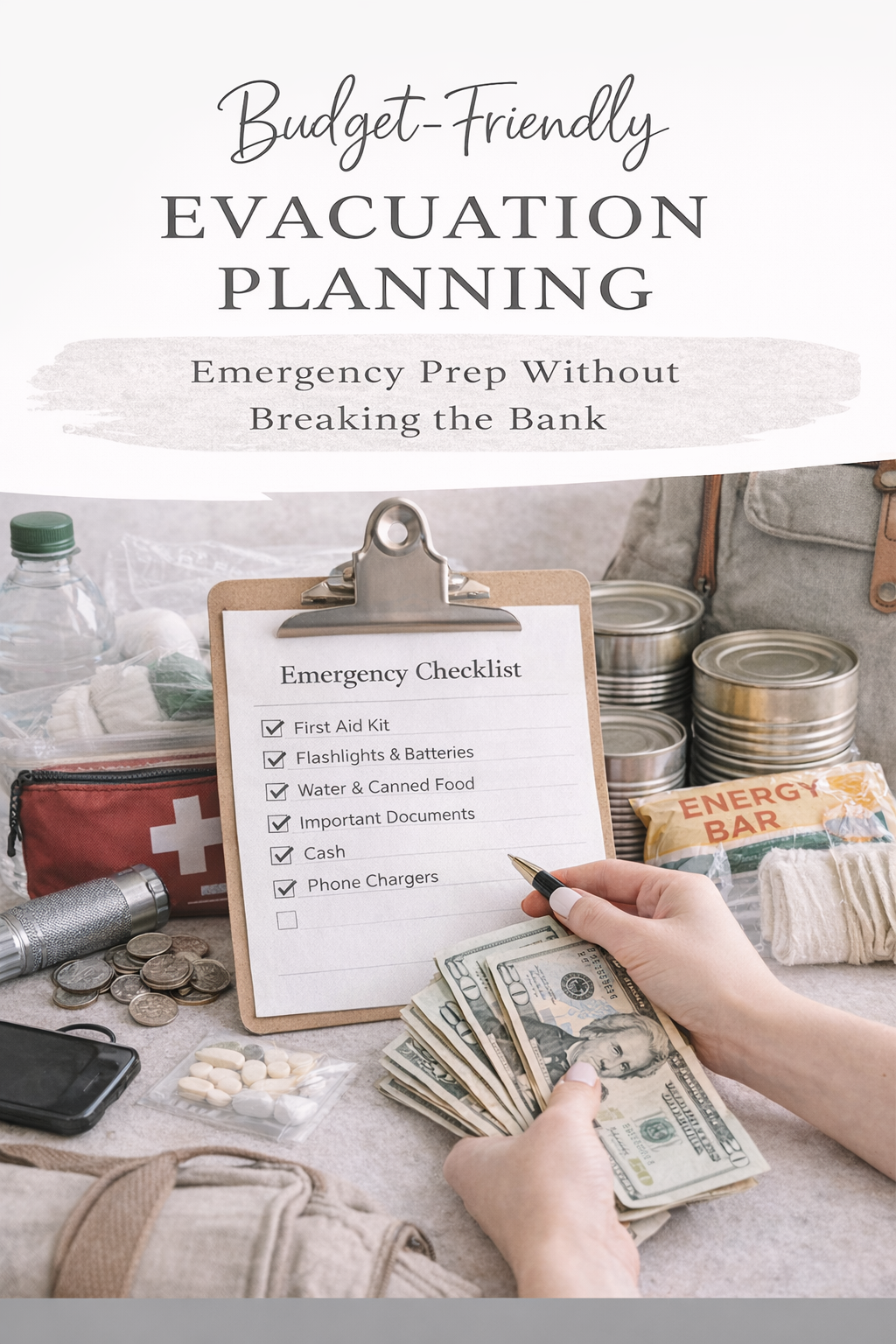

4) Assemble Your Financial Go-Bag

Envision a small, portable bag that stays in a safe spot—ready to be snatched up the moment you have to leave the house unexpectedly. The concept is similar to a typical “go-bag” used for natural disasters, but this one is all about your financial lifelines.

What Goes Into A Financial Go-Bag?

Here’s a quick table outlining common items to include:

| Item | Purpose |

|---|---|

| Basic Cash | A small stash for immediate expenses (e.g., gas) |

| Key Documents | Copies of IDs, insurance cards, key phone numbers |

| Emergency Fund Details | Info on accessing your emergency savings quickly |

| Checkbook & Spare Debit Card | For important payments if digital access is limited |

| USB Drive With Digital Files | Password-protected backup of crucial records |

| Contact List | Family, friends, doctors, insurance, and more |

Keep expensive valuables or large amounts of cash tucked away separately in a more secure location. This bag is meant for quick escapes—like if there’s a forced evacuation, a home fire, or another crisis that requires you to leave your home on short notice.

Safety First

- Choose A Fireproof Bag

If possible, get a bag that’s water-resistant or fireproof. Emergencies rarely come with warnings, and physical protection for your documents can be a game-changer. - Keep It Hidden

Store the bag somewhere discreet but accessible. This is especially important if you live in a multi-person household or have frequent visitors. - Review Its Contents

Make sure you rotate out any expired IDs or cards. Keep all phone numbers, account passwords, and URLs up to date.

Having a dedicated, well-stocked go-bag ensures that even if you can’t stay home during a crisis, you won’t be without the critical pieces of your financial puzzle.

5) Compile A Secure Binder

Think of a financial emergency binder as the big sister to your go-bag. While the bag is your “grab on the run” solution, the binder is your comprehensive reference center—perfect for storing more detailed financial information that you might not need immediate access to in a crisis but will definitely want at your fingertips once the dust settles.

Assembling The Binder

This binder should be separate from your day-to-day filing system. Use sturdy dividers to categorize documents so you can find what you need quickly. For easy navigation, consider sections like:

Banking & Credit Cards

- Account numbers, interest rates, and contact details

Investment & Retirement

- Statements, beneficiary info, and broker contacts

Insurance Policies

- Policy numbers and coverage summaries

Bills & Utilities

- Account login details, payment history, and due dates

Estate Planning

- Wills, power of attorney, and advanced healthcare directives

Going Digital vs. Paper

Storing all of this in a paper binder is great for tangibility, but digital backups can also come in handy. You might keep scanned PDF copies, protected with passwords, in a secure cloud service. That way, you’ll have a fallback if the physical binder gets damaged or misplaced.

Tips For Minimizing Risk

- Use Non-Glare Page Protectors

Page protectors safeguard documents from spills and frequent handling. - Lock It Up

If you can, keep the binder in a locked drawer or cabinet. Alternatively, use a small locked box for an extra security layer. - Share Wisely

Inform a trustworthy family member or friend about the binder—especially where you store it—so you have a backup plan if you’re not around to retrieve it.

Your binder acts like a map for your overall financial situation, ensuring all critical details are neatly laid out. When a crisis pops up, you’ll be glad this binder is there, helping you navigate your finances without the usual scramble.

6) Set Aside Accessible Cash

Picture this scenario: the power is out in your neighborhood, and credit card machines are down. Maybe you need extra gas or a few basic groceries. When the technology that powers digital payments isn’t working, that old-fashioned paper money becomes king again, at least temporarily. Storing emergency cash at home is a big plus in your financial emergency preparedness kit. It ensures you’re never left helpless if your debit card or phone payment app can’t process transactions.

How Much Cash Is Enough?

There’s no one-size-fits-all answer. You might aim for at least a few hundred dollars in smaller denominations (like $20s, $10s, and $5s). Enough to handle a night in a motel if weather conditions force evacuation, fill your gas tank, or buy groceries for a few days. If you have a large family, you might store a bit more.

Best Practices For Storing Physical Cash

- Choose A Discreet Spot

Lockboxes, safes, or hidden home compartments are your friends here. Make sure it’s not too obvious, and be mindful of factors like fire or water damage. - Rotate Bills

Bills can degrade over time, especially if exposed to humidity or moisture. Doing a quick check every six months helps keep your stash in good shape. - Combine With Digital Options

Even though cash is crucial in some scenarios, keep a portion of your overall emergency fund in a bank. That way, you have multiple ways to pay in different situations.

Accessible cash can be a lifesaver in sudden or natural disasters when electronic payment systems go down. Combined with your other savings strategies, a little bit of paper money in hand can make a huge difference.

7) Plan For Debts And Insurance

Your financial emergency preparedness kit isn’t just about saving or storing documents. It also involves tackling existing financial obligations—like debts or insurance premiums—in a way that won’t leave you floundering if times get tough.

Handling Debts Proactively

- Prioritize High-Interest Debts

Debts with high interest rates, especially credit cards, can spiral quickly when you’re tight on cash. Try chipping away at those balances first or consider a 5 savings challenge approach where you steadily reduce what you owe. - Set Up Payment Strategies

If an emergency hits and you can’t meet a payment, contact your creditor immediately to discuss possible arrangements. Many lenders offer hardship programs if you’re proactive.

Insurance: A Cushion For The Unexpected

Health insurance, life insurance, homeowner’s or renter’s insurance, disability coverage—they all protect you from massive bills. Think of them as guardrails that help your finances bounce back faster. If you’re unsure which types you really need, consider anything critical to your family’s long-term well-being. For instance:

- Health Insurance

Even with a modest policy, you reduce the risk of facing astronomical medical bills. - Life Insurance

This becomes more important if people rely on your income or if you’re a caregiver. - Disability Insurance

Helps replace a portion of your income if you get injured or develop a long-term illness.

Keeping A List Of Policies

Organize your insurance information in the binder we talked about above, or keep an updated digital note you can pull up quickly. Having the policy numbers, coverage amounts, and contact information at your fingertips lets you file claims or make adjustments much more smoothly.

Many of us pay our monthly premiums and rarely look at the fine print. In an emergency, though, understanding what your insurance covers can determine whether you’re shelling out thousands out of pocket or getting the help you need. By planning for debts and insurance in tandem, you ensure that your finances stay balanced—even when life throws a curveball.

8) Revisit And Update Regularly

Here’s the thing about life: it doesn’t stand still. Families grow, jobs change, new bills pop up, and old expenses fade away. What worked for your emergency plan last year might not fit your life today. This twisty-turny nature of adulthood makes regular check-ins a must.

Schedule Your Check-Ins

Try setting a recurring date—about once or twice a year—to give your emergency prep a thorough makeover. This can align with key times, like tax season or a birthday month, so you won’t forget. During these check-ins, you’ll want to:

- Update Your Documents

Replace any missing or outdated paperwork. If you’ve recently bought a new car or changed jobs, factor that in. - Tweak Insurance Policies

Have your needs changed? Maybe your health plan needs an upgrade if you’re expecting a child, or your homeowner’s coverage should expand if you’ve remodeled the house. - Adjust Your Fund Contributions

If you got a raise or changed your monthly budget, consider increasing (or even lowering) automatic transfers to your emergency fund guide.

Avoid Common Pitfalls

- Forgetting Your Passwords

Keep a secure system (like a password manager) so you can access digital records without being locked out at the worst time. - Neglecting Critical Updates

Did you recently get married, divorced, or have a child? Don’t forget to update your beneficiary information on life insurance and bank accounts—often overlooked! - Overconfidence

Feeling like you’re set for good can lead to complacency. Remember, emergencies don’t send an invitation. Stay ready.

Refreshing your financial emergency preparedness kit is like routine maintenance on your car. It keeps you one step ahead of unpleasant surprises. You’ll thank yourself later for staying vigilant.

9) Embrace Long-Term Success

Okay, so you’ve organized your binder, saved up a dedicated emergency fund, tucked away some physical cash, and covered your bases with insurance. That’s a lot to celebrate. But just like any important journey—whether it’s embarking on a new fitness routine or learning a new skill—your financial wellness needs ongoing care and a forward-thinking mindset.

Continual Learning And Growth

Your relationship with money will keep evolving. As you gain confidence, you may want to experiment with bigger saving challenges or explore new ways to prepare for inflation. Strengthening your financial health isn’t about reaching one finish line; it’s about keeping an outlook that embraces learning and growth at every stage.

- Consider Future Goals

Are you eyeing a college fund for your kids or a goal to retire early? Once your emergency footing is solid, shift some attention toward these goals. Each new milestone builds on your financial stability. - Stay Motivated With Community

You don’t have to do all of this alone. You might join an online budgeting group, swap saving tips with friends, or check in occasionally with a financial coach. Accountability can make all the difference. - Reward Yourself Wisely

Whenever you meet a big target—like hitting your ideal emergency fund amount—treat yourself in a meaningful but budget-friendly way. Think an afternoon picnic with the family or a mini spa day at home. You earned it.

Shifting Your Mindset

When you first start out, the concept of building an emergency fund, organizing a binder, and analyzing debt can feel overwhelming. But as these tasks become second nature, you’ll notice a new kind of confidence trickling into other spheres of your life. That’s the hidden gem of financial preparedness: knowing you’ve got your own back when storms come your way.

Most of all, remember that progress is a series of small steps. If you ever feel like you’re veering off-course—maybe an unexpected bill derails your saving plan—know that you can pivot and rebuild. For instance, if you use some of your emergency stash, you can rebuild emergency fund balances in stages. These moments aren’t failures. They’re natural parts of your journey, shaping you into someone who can handle whatever life tosses in your path.

Bringing It All Together

Look at you, putting together a robust safety net. From clarifying your big “why” to laying out important documents, you’re crafting a plan that will make a real difference when surprises come knocking. This isn’t about aiming for perfection—it’s more about ensuring you have a roadmap, a reliable go-bag, a binder full of relevant details, and a cash cushion ready to support you.

Think of everything we’ve covered here as puzzle pieces that fit into your custom financial emergency preparedness kit. Each piece has a different role, but collectively, they give you holistic coverage to face the unexpected. And the best part? You don’t have to do it all in one weekend. Start with the most pressing need—maybe that’s building a 1000 emergency fund—and gradually introduce the other components into your life.

We all want financial peace of mind, especially when we’re looking after our children, supporting aging parents, or juggling everyday responsibilities. Life is plenty stressful on its own, but having a well-thought-out strategy removes a huge portion of the worry about “What if?” Trust me, you’re not alone on this path. We’re all carrying our own blend of fears, hopes, and dreams, and a strong financial foundation helps lighten the load.

So here’s to you, taking these steps at your own pace. Give yourself credit for prioritizing future security—no matter how many times you adjust or pivot along the way. In truth, small actions today can compound into significant stress relief tomorrow. Plus, as someone who’s been through her share of financial ups and downs, I can assure you this: once you feel the confidence that comes from being prepared, you’ll wonder how you ever managed without it.

Keep going, keep learning, and keep refining. You’ve got a long road ahead, but with each careful addition to your financial toolkit, you’re positioning yourself and your loved ones for a more secure, steady life. And that, my friend, is worth every bit of effort.