The Complete Financial Preparedness Checklist for Families

If you’re looking for a financial preparedness checklist that suits your family’s real-life needs, you’re in the right place. It’s easy to feel overwhelmed when you hear terms like “emergency fund,” “insurance coverage,” or “estate planning.” Trust me, we’ve all been there—juggling responsibilities, caring for loved ones, and trying to stay afloat when unexpected expenses pop up.

But here’s the bright side: taking a proactive approach to your finances doesn’t have to feel like an epic undertaking. Think of this as a friendly guide, with us walking step by step through each piece of your financial safety net. Everything from establishing an emergency fund to organizing crucial paperwork, all while keeping things low-stress and family-friendly. Because at the end of the day, we’re in this together, and together we can create a plan that fits your life.

Below, you’ll find practical strategies, encouraging stories, and supportive tips to help you gain a sense of security about your money. We’ll talk about handling daily expenses, dealing with debt, and preparing for the unexpected, so you can focus on what matters most—enjoying time with your family.

Evaluate Your Financial Picture

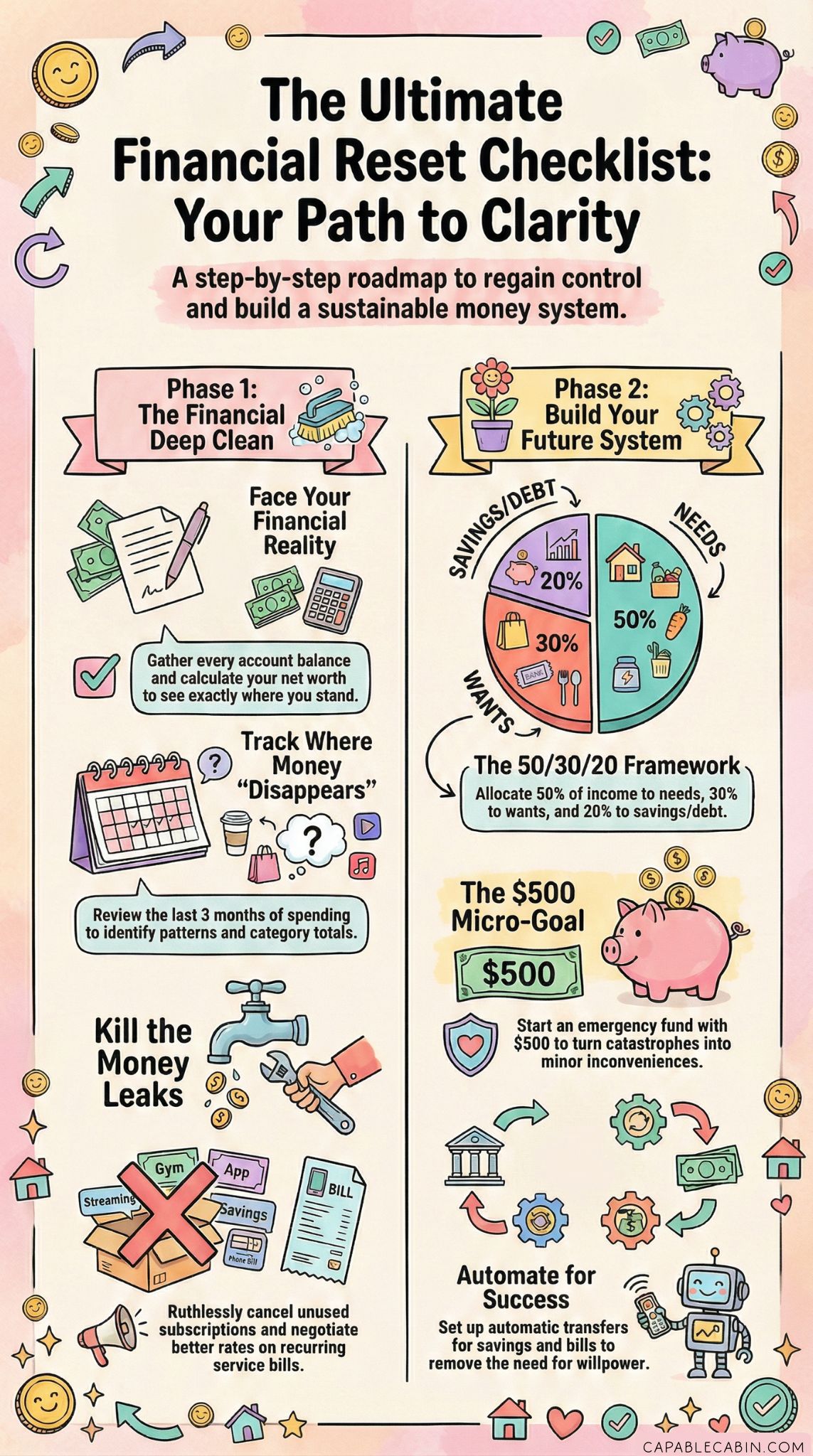

Before we start layering in new goals, it helps to assess where you stand today. Think of it like cleaning out your pantry before stocking it with fresh ingredients. You want to see what you’ve already got and what might be missing. In this step, you’ll piece together a clear snapshot of your financial life, which lays the foundation for more specific tasks later.

Track Daily Spending

One of the simplest moves you can make is tracking your daily expenses. From groceries to coffee runs, it’s easy for small costs to pile up, often without you even noticing. Grab a small notebook or open a spreadsheet, and for a few weeks, jot down every single purchase. When you see those amounts in black and white, patterns become more obvious—like that latte that’s quietly chipping away at your budget every morning.

Don’t feel guilty if you discover you’re overspending in some areas; awareness is a powerful first step. Once you know where your money actually goes, you can make little tweaks here and there. Maybe you kick the extra takeout habit, or set a limit on streaming subscription add-ons. Every decision, no matter how small, adds up in the long run.

Note All Income Sources

Next, evaluate your income streams. Your primary paycheck might be the main source, but do you have income from side gigs, freelancing, investments, or rental properties? If you have a partner, map out their contributions as well. Listing each source helps you understand your combined monthly cash flow, which we’ll need later when we talk about budgeting and saving.

If you spot opportunities to bring in more money—perhaps by doing part-time contract work or selling crafts online—jot those ideas down too. Not everyone wants or needs multiple income streams, but it’s worth noting where flexibility might exist. After all, financial preparedness is also about being open to new ways of boosting your savings cushion.

Identify Your Debt

One more critical aspect of your current snapshot is the debt you carry. This includes credit cards, car loans, student loans, mortgages—any type of debt. Note the balance on each, the interest rates, and the monthly minimum payments. Debt can weigh heavily on your peace of mind, so we want to keep it front and center as we move forward with our plans. You might also set aside time each month to explore whether consolidating debt or refinancing loans could make sense for you.

This initial assessment might feel like an information overload, but don’t stress. It’s like sorting the pieces of a puzzle: once you know what you’re working with, it becomes easier to craft a plan that keeps your family on track.

Secure an Emergency Fund

Securing an emergency fund is the bedrock of any financial preparedness checklist. Why? Because having readily available savings can be a lifesaver when life throws a curveball—like an unplanned medical bill, car repair, or job loss. This fund is your safety net, helping you avoid high-interest debt (such as credit cards) and maintain stability.

Why an Emergency Fund Matters

An emergency fund acts like a cushion between you and life’s ups and downs. Without it, a single unexpected expense like a broken furnace in winter might force you into debt. Sometimes, you might dip into your fund for something as small as covering a copay or as big as replacing a major appliance. Either way, you won’t have to scramble, stress, or rely on high-interest options.

If you’re wondering how much to set aside, some experts recommend three to six months’ worth of living expenses. Others suggest starting with a smaller initial goal, like 1000 emergency fund, then building up incrementally over time. The exact number will vary, but the main idea is to get started so you have something set aside, even if it’s just a few hundred dollars right now.

Exploring Different Approaches

We all have different personalities and lifestyles, so it helps to find a savings strategy that matches yours. Here are a few popular methods you might consider:

- Starter Emergency Fund: Some families find it helpful to begin with a modest amount—$500 to $1,000—to cover small emergencies. Once you hit that goal, build on it step by step.

- 5 Savings Challenge: This approach involves saving a small, manageable amount every day, week, or month. You regroup regularly to track your progress, celebrate wins, and gradually increase your daily or weekly savings as you become more comfortable.

- Year-Long Emergency Fund Challenge: This is more structured and may involve a formal plan, like putting away a set amount every month to reach a specific figure by the end of the year.

- Emergency Fund Envelope System: If you’re a fan of physical cash, consider dividing your money into labeled envelopes—like “essentials,” “fun,” and “emergency”—so you can visually see how much is allocated.

No single approach is superior to the others; it’s all about what resonates with you. If you prefer the thrill of a challenge, a daily or weekly savings game might motivate you. If you want something straightforward, an automatic monthly transfer to a dedicated account will do the trick.

Where to Keep Your Savings

It’s key to keep your emergency fund accessible, but not so easy to dip into that you’re tempted to use it for non-emergencies. Many families use a high-yield savings account, which typically allows free transfers while offering a bit more interest than a standard checking account. If you want advice on storing your savings wisely, check out our tips in where to keep emergency fund. The main point is, you want your emergency money available fast when you really need it, without burying it so deep that it’s a hassle to get to.

Pitfalls to Avoid

One common pitfall is treating the emergency fund like “just another savings bucket.” Consider labeling the account “Emergency Fund” so you’re less likely to blur the lines. Another stumbling block is failing to replenish the fund after you use it. Emergencies happen, and once you see that balance drop, remind yourself to build it back up as soon as possible. If you need more tips on replenishing after an unexpected withdrawal, rebuild emergency fund can help.

The Bottom Line

At the end of the day, your emergency fund should feel like a soft landing spot. Even if it’s not huge right now, you’re taking the first steps toward greater security. Over time, it grows into a safety net that spares you from last-minute scrambling when life surprises you. You’ll likely find that, once you get used to having an emergency fund, your overall stress level decreases—simply because you know you have a fallback plan.

Organize Vital Documents

A strong safety net goes beyond just having money. It includes being able to access the right documents when you need them. Having everything neatly gathered is especially important if you ever face an urgent situation—like evacuating during a natural disaster or rushing to the hospital. The last thing you want is to hunt through piles of paperwork at the worst possible time.

Build a Financial Binder

Consider creating a dedicated binder or folder—sometimes called a financial emergency binder. This binder could include:

- Copies of IDs (driver’s licenses, passports)

- Bank account information

- Insurance policies

- Loan and credit details

- Retirement account statements

- Contact info for financial institutions and advisors

- Important family documents (birth certificates, marriage certificates, wills)

Label everything clearly, and keep it in a safe but accessible place. You can even slip each document into a plastic sleeve for protection from spills or minor wear and tear. If you’re wondering whether you should store them digitally, that can be a great backup plan—just remember to keep your digital files encrypted and password-protected.

Assemble a Financial Go Bag

If you ever need to leave your home quickly, a financial go bag ensures you have essential documents at your fingertips. This could be a small, fireproof box or pouch. It’s also wise to include a bit of emergency cash at home, just in case ATMs or electronic payments become inaccessible. You never know when a power outage or a natural disaster might interrupt electronic banking systems.

Digital vs. Physical Storage

There’s a lot of debate about whether digital copies are enough. Ultimately, having both physical and digital storage solutions can be your best bet. Printed copies help if your laptop battery dies or you lose internet service, while online backups protect you from house fires or floods. You don’t have to do everything all at once—scan a few documents a week as you have time, then gradually build up a complete digital repository. You can learn more about secure digital filing in emergency financial information storage.

Understand Insurance Options

Insurance can sometimes feel confusing, but it’s essentially designed to shield you financially when life happens. From a health crisis to a house fire, the right plans can prevent catastrophic losses. The key is to ensure you have proper coverage without paying for what you don’t need.

Health Insurance

Health expenses are often at the top of the list of unexpected costs that can derail a budget. Evaluate your health insurance plan carefully. Does it cover major procedures, prescriptions, or specialist visits? Are you paying more out of pocket than you’d like? If your current coverage isn’t meeting your family’s needs, explore other options during open enrollment or consider a supplemental plan that bridges the gaps.

Property and Life Insurance

If you own a home, make sure your homeowner’s insurance covers natural disasters common in your area, whether that’s earthquakes, flooding, or hail. Renters should confirm that their policy covers personal belongings in case of fire or theft.

Life insurance can offer essential reassurance for families, especially if you have children. You want to ensure that if something unexpected happens to you or your spouse, your loved ones remain financially secure. Term life insurance policies are usually more affordable than whole life; consider discussing options with a trusted professional who can give you a breakdown of what fits your budget and goals.

Disability and Other Specialty Policies

Maybe you have a job that comes with certain risks, or you’re self-employed and worry about potential injuries. In those scenarios, disability insurance could be a smart addition. Some families find umbrella policies helpful too, which provide extra coverage for large liability claims. While none of us plans to be in an accident or face a lawsuit, insurance helps you avoid draining your finances if something goes wrong.

Plan for Medical Expenses

Medical bills often pop up when you least expect them—a sudden infection, emergency surgery, or even that random trip to urgent care for a sprained ankle. Having a plan in place can ease a lot of anxiety when health issues arise.

Consider an HSA or FSA

If you have a high-deductible health plan, a Health Savings Account (HSA) can be a cost-effective way to set aside funds for medical expenses. HSAs offer tax advantages, and the money rolls over from year to year if you don’t use it all.

On the other hand, a Flexible Spending Account (FSA) lets you set aside a specific amount of pre-tax dollars for qualified healthcare costs. One caveat is that most FSAs are “use it or lose it,” meaning the money might not roll over entirely. So, you’ll want to estimate your yearly medical expenses carefully.

Budget for Routine Care

Regular checkups and preventative services can save a fortune down the road. Routine cleanings at the dentist, well-child visits, and eye exams often catch problems early. Set aside funds for these “smaller” healthcare costs, which helps you avoid feeling blindsided by appointment fees or prescriptions.

Negotiate and Shop Around

Many people don’t know you can shop for medical services. For non-urgent procedures, compare prices at different clinics or hospitals. If you receive an unexpectedly high bill, contact the billing department to see if there’s room to negotiate or set up a payment plan. You’d be surprised how often a friendly phone call can reduce your financial burden, especially if you express genuine concern and need.

Discuss Estate Planning

Planning for what happens after you’re gone may feel heavy, but it’s a gesture of love and care toward those you leave behind. When your family knows exactly what your wishes are, they can navigate a difficult time without extra financial distress or confusion.

Wills and Guardianship

If you have children, naming a guardian in your will is crucial. It ensures your kids are raised by someone you trust if something happens to you and your partner. Even if you think you don’t have many assets, a will clarifies how your property—no matter how modest—should be distributed.

Advanced Healthcare Directives

An advanced healthcare directive or living will spells out your medical preferences if you can’t speak for yourself. It’s not a fun topic, but imagine how relieved your loved ones will feel, knowing they are honoring your exact wishes. These documents reduce guesswork and guilt when difficult choices arise.

Beneficiaries and Trusts

Regularly review the beneficiaries listed on your accounts—like 401(k)s, life insurance policies, or bank accounts—so they always match your current wishes. If you have complex assets or a large estate, you might benefit from a trust, which can offer tax advantages and smoother management of your assets. This is definitely a discussion to have with a qualified estate attorney if you’re unsure.

Diversify Income Streams

Relying on a single income source can be a bit nerve-wracking. If your primary job wobbles due to economic shifts or layoffs, it’s good to have another way to keep money coming in. While not everyone has the time or interest to juggle multiple jobs, exploring different income possibilities can add a layer of resilience to your plan.

Ideas for Supplemental Income

- Freelancing or consulting if you have specialized skills (writing, graphic design, bookkeeping)

- Selling homemade products online, like crafts or baked goods

- Offering lessons or tutoring in a subject you’re skilled at, such as music or languages

- Renting out a spare room or your entire home occasionally (if local regulations allow)

- Participating in the gig economy by driving for a rideshare or delivering groceries

Partnering on Family Projects

Sometimes, turning a family hobby into a small side hustle can bring in extra income while also strengthening your bond. For instance, if you and your kids love baking, you could start a booth at a local farmer’s market. Just remember to check local laws and see if you need permits. Even modest profits can make a real difference when you’re building a financial cushion or paying off debt.

Finding the Right Balance

While boosting income can be a game-changer, it’s also important to avoid burnout. We all have our limits, and overcommitting can strain your physical health, mental well-being, and family time. Aim for treading that comfortable middle ground—earning a bit extra without sacrificing too much balance. You’ll sense when you’re hitting your sweet spot.

Protect Your Credit

Credit might be a double-edged sword: it helps you acquire big-ticket items like a home or a car, but it can lead to debt if not managed carefully. Maintaining good credit means lower interest rates on loans, which ultimately saves you money.

Check Your Credit Reports

In many places, you can request at least one free credit report per year from each of the major credit bureaus. Reviewing these reports can help you spot errors or signs of identity theft. If you find any discrepancies—like accounts you never opened or balances that don’t match your records—dispute them right away. Cleaning up mistakes can boost your score, making it easier and cheaper to borrow when you truly need it.

Keep Credit Card Balances in Check

It’s easy to swipe a card for everyday expenses, but try not to carry a large balance. Interest charges can add up fast, taking a bite out of your monthly resources that could go to savings or an emergency fund. Aim to pay off your credit card bills in full each month. If that’s not feasible, focus on paying more than the minimum so you chip away at your balance faster.

Consider a Credit Freeze or Fraud Alerts

If you rarely apply for new credit, a credit freeze can lock your reports from being accessed unless you lift the freeze with a personal PIN. This makes it harder for identity thieves to open cards in your name. Frauds or data breaches can happen to anyone, so a little proactive measure can save a lot of trouble down the line.

Create a Household Budget

A budget is your road map—it shows you how much money is entering your household, where it’s going, and how you can allocate resources to fit your family’s needs. If you’re not used to budgeting, don’t worry. Once you lay it all out, you’ll likely feel more in control.

How to Structure Your Budget

Everyone’s budget looks a little different, but a simple model might include these categories:

- Housing (rent or mortgage, property taxes, basic utilities)

- Transportation (car payments, fuel, public transit)

- Food (groceries, occasional dining out)

- Healthcare (insurance premiums, co-pays, medications)

- Debt Payments (credit cards, loans)

- Savings (emergency fund, retirement, short-term goals)

- Discretionary (entertainment, hobbies, gifts)

You can craft a table to see these categories side by side:

| Category | Monthly Budget | Actual Spent | Difference |

|---|---|---|---|

| Housing | |||

| Transportation | |||

| Food | |||

| Healthcare | |||

| Debt Payments | |||

| Savings | |||

| Discretionary | |||

| Total |

Consider adopting a zero-based budget approach, where every dollar is assigned a “job,” even if that job is saving. This method ensures you know exactly how your paycheck is distributed.

Envelope System for More Control

If you like tangible methods, check out the emergency fund envelope system. While it’s typically associated with saving for emergencies, the same logic can be applied to your entire budget. Label envelopes for each category, and place the allotted cash in each envelope at the start of the month. Once the money in a certain envelope is gone, that category must wait until next month for more funding. It can be an eye-opening experience that trains you to pace your spending.

Adjusting for Real Life

Let’s be honest, budgets aren’t static. Kids grow out of clothes faster than you’d imagine, grocery prices fluctuate, and unexpected invites to birthdays or events come up. It’s perfectly fine to shuffle some categories around. The goal isn’t to whip yourself into financial shape overnight but to build awareness and direct every dollar toward what matters most to your family.

Keep the Plan Updated

Your life today may look entirely different in a year. Perhaps your toddlers become school-age, your job situation changes, or you decide to move. That’s why it’s important to review and adjust your financial preparedness plan regularly.

Schedule Regular Check-Ins

Set aside one evening every quarter (or at least twice a year) to review everything. During these check-ins, ask yourself:

- Do we still have the right level of emergency savings?

- Has our insurance coverage changed or do we need updates?

- Have we added any new debts or paid off old ones?

- Are our documents still accurate?

- Do we need to tweak the budget?

Updating your plan doesn’t have to be a long, drawn-out affair—sometimes 30 minutes is enough to get everyone on the same page. If you have a partner or older kids who want to be involved, bring them in. This keeps everyone invested in the family’s financial well-being.

Celebrate Progress

When you see improvements—like paying down a chunk of debt or noticing your savings have grown—celebrate. It doesn’t have to be an extravagant party, but a simple acknowledgment goes a long way. Even giving each other a high five or making a favorite dessert can reinforce that you’re moving in the right direction.

Build a Support Network

Going it alone can feel isolating, especially if finances are a stressful topic in your home or community. Reaching out for help or simply chatting with supportive friends can boost your confidence and keep you accountable to your goals.

Share Goals With Friends and Family

Tell close friends or family members about your plan to build an emergency fund or pay down debt. They might have tips or resources, or they could even become your “finish line cheerleaders.” If you’re working specific challenges like the emergency fund challenge, having a buddy who’s doing it too can be empowering.

Seek Professional Advice

Sometimes, you might need specialized help. If taxes, insurance, or investments feel like uncharted territory, a certified financial planner or a trusted advisor could simplify the process. Asking for guidance saves you time and frustration, and it can prevent costly mistakes.

Local Community and Online Groups

Check for community workshops at a nearby library or community center. These free events often cover topics like budgeting, credit repair, or even how to start an emergency fund vs savings. Online forums and social media groups can also offer camaraderie—you can ask questions, share experiences, and pick up clever budgeting hacks. Just remember to verify the information you find in online spaces and prioritize advice that’s consistent with your personal values and situation.

Conclusion

Building a financial preparedness checklist isn’t about creating a rigid set of rules you’ll forever stress over. It’s about giving yourself and your family a sense of security and freedom so you can focus on the moments that truly matter. When you know you have an emergency fund in place, your vital documents organized, insurance lined up, and a clear budget to follow, life’s curveballs start to feel more manageable. You won’t be stuck wondering if you can afford an unexpected car repair or a medical emergency—you’ll already have a plan.

Remember that no one’s journey here is flawless, and there’s no “perfect” time to get started. You might find yourself toggling between paying down debt one month and building savings the next, or you might dip into your fund when something truly requires it and then replenish it when things stabilize. That’s normal. The goal is progress, not perfection.

Above all, rest easy knowing that, step by step, you’re strengthening the financial backbone of your family. Every little move—tracking daily expenses, automating a small deposit into your emergency fund, updating a will, or reviewing your insurance coverage—brings you closer to a secure, prepared future. So keep cheering yourself on and embracing the next step in your plan. You’ve got this, and you’re not alone in the journey. Our community is right here, cheering you on to a more confident and stable tomorrow.