Evacuation Insurance Claims: Financial Recovery After Disaster

Life can take some sharp turns when you least expect it. One moment, everything seems calm, and the next, you’re rushing to pack your essential documents, gather the kids, and make sure everyone stays safe. If you’ve ever found yourself wondering how to protect your family’s finances in the face of a sudden evacuation, trust me, you’re not alone. That’s where evacuation insurance claims can play a huge role in helping you bounce back and cover those unexpected costs. Let’s take a thorough look at how you can prepare, file claims effectively, and recover financially after disaster strikes. We’re in this together, and by the end of this guide, you’ll have a clearer picture of how to safeguard your money—and your peace of mind—when it matters most.

Because this topic involves so many moving parts, we’ll break it down into practical steps you can follow. You deserve guidance that doesn’t feel intimidating or complicated. Whether you’re planning for wildfires, hurricanes, floods, or any other crisis, a bit of well-placed preparation can save you so much time, stress, and money in the long run. Let’s walk side by side through the details, from why this type of insurance matters to how you can keep track of every claim-related document. By the end, you’ll be that much closer to feeling financially secure in the midst of chaos.

Reflect On The Importance

Sometimes, we don’t realize just how fragile our normal routines can be until a crisis knocks at our door. You might be wondering if specialized evacuation insurance is necessary at all. After all, many of us already have some kind of property or health coverage. But here’s the thing—standard insurance policies often aren’t enough to handle abrupt evacuations or unexpected out-of-pocket costs that arise in a hurry. Even if you have a comfortable savings cushion, the costs can add up faster than you think.

- Lodging and Meals: Finding a hotel at the last minute or buying last-minute groceries can skyrocket expenses.

- Emergency Transportation: Flights, rental cars, or even extra gas for a long-distance drive are rarely cheap.

- Medical Care Away From Home: If anyone in your household has medical needs, you may have to cover extra expenses for prescriptions, therapy, or emergencies on the road.

- Rebuilding or Temporary Housing: Sometimes, returning to your home is impossible right away. You may need a longer-term solution if your house was severely damaged.

One of the best ways to make sure you’re not facing those expenses alone is through an insurance policy specifically designed to address evacuation-related costs. The claims process provides the reassurance that, in a pinch, you won’t completely drain your bank account. Ultimately, it’s about feeling supported and knowing that someone’s got your back when you have to leave home in a hurry.

Recognize Different Insurance Types

When we talk about financial security during an evacuation, it’s essential to understand that there isn’t a one-size-fits-all approach. Policies can vary widely depending on your region, the type of disaster risk you face, and whether you’re traveling or staying near home. Let’s look at some popular coverage types that could come into play:

- Property Insurance (Homeowners, Renters): Offers protection for damage to your home or belongings, but may not automatically cover all evacuation costs.

- Travel Insurance: Useful if you’re away from home (say, on vacation or business trips) and need to evacuate suddenly.

- Disaster-Specific Insurance: Some insurers offer specialized coverage for floods, earthquakes, hurricanes, or wildfires, which can often include evacuation-related expenses.

- Business Interruption Insurance: If you run a small home business, you might want coverage that helps compensate for lost income when you can’t operate due to mandatory evacuations.

- Medical Evacuation and Repatriation: Typically geared toward those traveling internationally, this can help cover emergency flights and medical transport fees.

Each policy’s fine print decides what’s covered and what isn’t. That’s why reading the details before a crisis hits is so important. If you’re unsure about whether your existing plan addresses evacuation costs, call your insurance company and ask for clarity. You might find you need an add-on or a separate policy altogether. That small conversation now can save you massive headaches later.

Prepare Before Disaster Strikes

We’ve all had those moments where we think, “I’ll figure it out when it happens.” But when disasters actually unfold, panic can take over. Being prepared ahead of time is a real game-changer. True preparedness often involves both a plan for where you’ll go if you have to evacuate and a strategy for how to handle bills, credit card payments, and day-to-day costs during your time away from home.

- Build a Dedicated Fund: If possible, set up an evacuation emergency fund that you only tap into during a crisis. Even a small amount saved regularly can add up and give you a bit of breathing room.

- Review Your Insurance Policies: Make a habit of revisiting your coverage each year, especially if your life situation changes (new job, relocating, adding family members).

- Create a Financial Crisis Plan: Draft a straightforward financial crisis action plan. This might include a list of all your bills, online banking credentials (stored securely), and key contact information.

- Stay Organized Digitally: Download any apps your insurer provides so you can quickly snap photos or scan documents if needed. Consider exploring evacuation digital finances for an in-depth look at protecting your accounts online.

While we can’t prevent emergencies altogether, that sense of readiness can make a huge difference in how you cope emotionally. You’ll know you have a structure in place, including insurance details and financial resources, to keep some semblance of normalcy while you ride out the storm—literal or figurative.

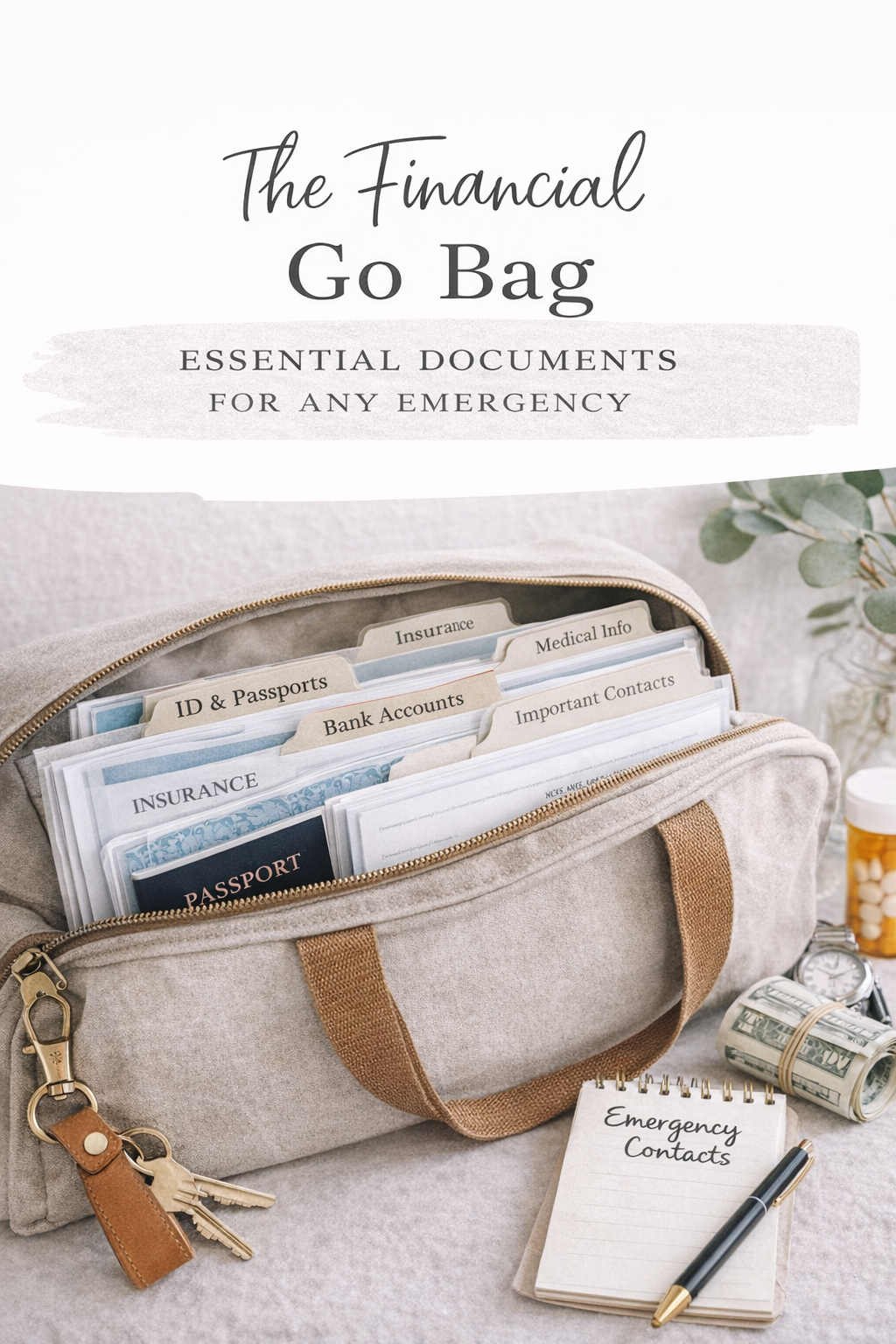

Collect Vital Documentation

Picture this: you’re rushing out the door with your kids, and there’s little time to think about paperwork. You grab a backpack, maybe throw in some water bottles, but you forget about your crucial insurance documents. Sounds stressful, right? That’s why it’s wise to gather everything you need long before a crisis hits.

Make a Documentation Checklist

- Insurance Policies: Keep copies of any relevant policies, along with your insurer’s contact information.

- Identification: Driver’s licenses, passports, Social Security cards—basically anything proving who you are.

- Property Records: Deeds or lease agreements can help show you have a legal interest in the property you’re vacating.

- Medical Records: Summaries of major procedures, current prescriptions, and doctor contact details are invaluable if anyone needs care while you’re away.

- Financial Summaries: Print or store electronically your latest bank statements, credit card info, and emergency contacts for quick reference.

Store these documents in a waterproof and fireproof container. Many people also create a financial evacuation go bag that’s easy to grab when leaving in a hurry. You might back up all these files digitally on a secure cloud platform or an encrypted USB drive. That way, if you can’t access the physical copies, you still have what you need to file evacuation insurance claims or prove ownership of your home and belongings.

File Your Insurance Claims

Throughout all the chaos, filing evacuation insurance claims can feel like one more chore—but it’s crucial for recouping your expenses. Let’s walk through how to tackle this process step by step:

- Contact Your Insurance Provider Immediately: As soon as you’re safe and have phone or internet access, notify your insurer about your situation. They’ll open a claim and explain any next steps.

- Document Everything: Keep receipts for lodging, meals, and transportation. Take photos or videos of any damage to your property before, during, and after the evacuation if possible.

- Fill Out Required Forms: Often, you’ll have to complete detailed statements about what happened. Be factual and thorough.

- Stay Organized: A simple way is to create a folder—digital or physical—where you store all claim-related paperwork, receipts, and correspondence.

- Follow Deadlines Strictly: Some policies require claims to be submitted within a certain window. Mark it on your calendar so you don’t accidentally miss it.

When the insurance adjuster gets involved, they might request additional information or schedule an inspection of your home once it’s safe. It helps to keep an open line of communication with them. Don’t be shy about asking questions: “What documents do you still need? Will there be a follow-up visit?” The goal is to ensure you’ve laid everything on the table so you can receive your rightful coverage.

Manage The Claims Process

Filing a claim is one thing, but actually seeing the process through to completion can be a different story. Sometimes the insurance company might need extra proof, or they might try to minimize their payout. It isn’t about creating friction, but rather ensuring both parties meet their obligations fairly.

- Maintain a Paper Trail: Save every email, letter, and note from phone calls. If you speak to a representative, jot down their name, the date, and the key points of the conversation.

- Consider Professional Help: In more complex cases (like major property damage or health complications), it might be worth consulting a public adjuster or attorney, especially if the insurer disputes your claim.

- Inspect the Payment Details: Once the claim is approved, carefully review the payment breakdown. Make sure it covers the categories promised in your policy.

- Review Financial Planning: While waiting for claim approval, it can be helpful to revisit budget evacuation planning so you can keep track of every expense.

If you hit a roadblock, try to stay calm. Yes, it’s frustrating, especially when you just want life back to normal. But remember, any additional paperwork requests or official queries might be their way of verifying your loss. Be prompt and thorough in your responses. This can speed up the entire process of receiving funds or reimbursement.

Handle Post-Disaster Finances

Let’s say the immediate crisis is winding down, and you’ve returned home, or maybe you’re in temporary housing while repairs happen. Now comes the next wave of financial considerations. From restocking groceries to covering home-improvement expenses, you could face a hefty bill even after insurance steps in. This is when a solid financial strategy becomes your best friend.

- Revisit Your Budget: You might have new expenses like higher utility costs, hotel fees, or storage unit rentals. Adjust your monthly budget accordingly.

- Seek Financial Recovery Resources: Explore financial recovery emergency fund strategies that can help you rebuild your savings or apply for emergency assistance programs.

- Look Into Relief Programs: Depending on where you live, federal or local resources might assist with repairs or living expenses. Don’t be shy about applying.

- Assess Any Debt: Sometimes, to fund immediate needs, families rely on credit cards or short-term loans. Keep tabs on those balances and prioritize paying them down as soon as you’re able.

If it feels overwhelming, that’s normal. Combine small wins with a forward-thinking mindset. Maybe you can freeze some discretionary expenses for a couple of months, or ask your credit card company for a temporary lower interest rate while you get back on your feet. We’re all in the same boat when it comes to adjusting to crisis-related costs, and every little step helps bring you closer to normalcy.

Seek Ongoing Support

Evacuations can leave emotional ripples long after you unpack your bags. It might feel like you’re constantly on edge, waiting for the next crisis. Financially, you could be dealing with bigger bills or brand-new challenges like property repairs, medical issues, or job disruption. During these times, leaning on supportive networks isn’t a sign of weakness—it’s a sign of strength.

- Community Tools and Workshops: Your local community center or non-profit might offer seminars on evacuation financial planning, budgeting, and more.

- Friends and Family: Don’t underestimate the value of simply asking for advice, be it about insurance, meal planning, or child care during an emergency.

- Online Forums and Groups: Many social media groups discuss everything from pandemic financial planning to coping with extreme weather evacuation. Sharing your situation or reading about others’ experiences can spark solutions you hadn’t considered.

- Professional Counselors: Speaking with a financial counselor or therapist can help you process the emotional toll and craft a balanced plan to move forward.

The key here is remembering you don’t have to go at this alone. Whether you seek out emotional support, professional expertise, or both, your stress levels can drop significantly when you share the weight of a tough situation. It’s like having a few extra sets of eyes and ears looking out for your best interests.

Embrace Long-Term Resilience

Once the dust settles, it’s tempting to breathe a sigh of relief and go back to business as usual. But if there’s one lesson every survivor of a crisis eventually learns, it’s that preparedness truly pays off. Making sure your evacuation insurance claims are well-documented and your finances are laid out clearly is only the start. Now’s the time to consider how you can strengthen your family’s resilience.

- Refresh Your Documentation: Replace any damaged paperwork. Update older copies with recent versions. This is especially important if your policy changes or you relocate.

- Expand Your Emergency Plan: Think about including new details like a safe place to store valuables or updated contact info for relatives who can help in a bind.

- Practice Evacuation Drills: Yes, it might feel a little silly. But walking through the process of gathering items, loading the car, or meeting at a designated spot can help everyone stay calm if you need to evacuate again.

- Review Coverage Yearly: Life changes—your family might grow, you could switch jobs, or the type of disasters common in your area could shift. Keep your insurance up to date.

This kind of forward-thinking approach not only helps you file future evacuation insurance claims more smoothly but also empowers you to adapt to whatever life tosses your way. It’s about leveling up from simply reacting in panic to having a solid plan you can rely on. You’ve seen firsthand how stressful an unexpected evacuation can be, and that experience can guide you to make even better decisions for the future.

Keep Your Momentum Going

At the end of the day, financial recovery after a disaster isn’t a straight shot forward. It’s full of twists and turns, moments of relief, and sometimes fresh dilemmas. Yet, every step you take—saving emergency cash, documenting your insurance details, or supporting your kids through the upheaval—is a little victory in itself.

And when it comes to evacuation insurance claims, consistency is key. Each claim you file, each phone call you make to your insurer, and each document you update bring you closer to securing the financial support you deserve. Yes, it can feel tedious sometimes, but keep going. You’re actively shaping a financial safety net that can make all the difference for you and your loved ones.

One more piece of encouragement: you’ve already made progress just by reading this far. You’re arming yourself with knowledge and strategies that countless people wish they had before a crisis. It’s like preparing a toolkit you can reach for whenever life throws a curveball. So let’s keep pushing forward—step by step, claim by claim, and plan by plan. You’ve got this, and you’re not alone.

No matter what natural disaster, health emergency, or unexpected event comes your way, know that you’re building a community and a strategy to guide you through. With every preparation you make now, you help ensure a smoother financial journey during and after the storm. Here’s to you, your courage, and the unwavering commitment to keeping your family’s finances on solid ground.